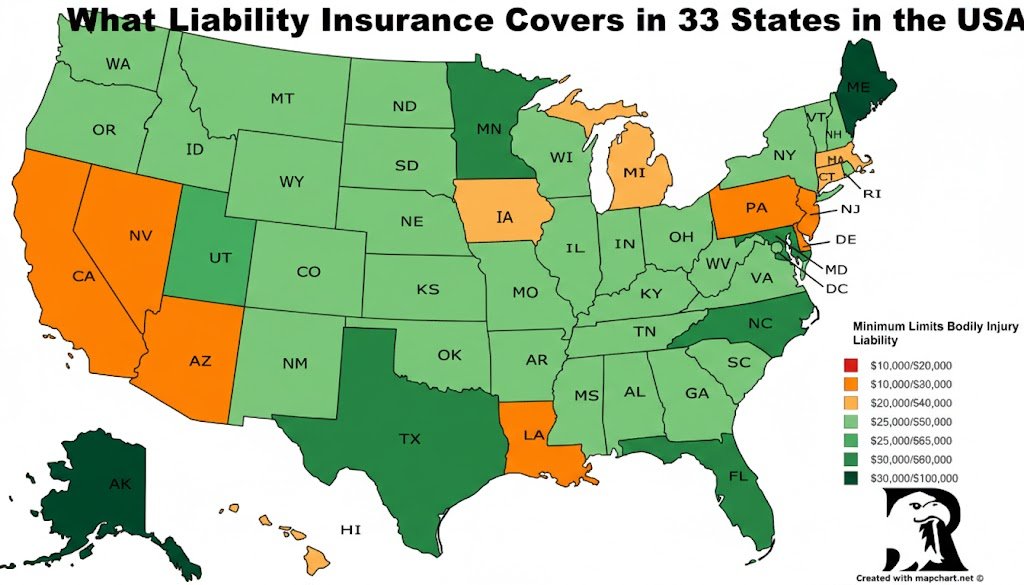

What Liability Insurance Covers in 33 States in the USA

Liability insurance serves as a financial safety net for residents and business owners across the United States. In the thirty-three states that follow specific tort or “at-fault” systems, this coverage is not just a suggestion; it is a legal pillar that ensures people are held accountable for accidents they cause. When you carry liability insurance, you are essentially protecting your future earnings and current assets from being seized to pay for someone else’s medical bills or repair costs.

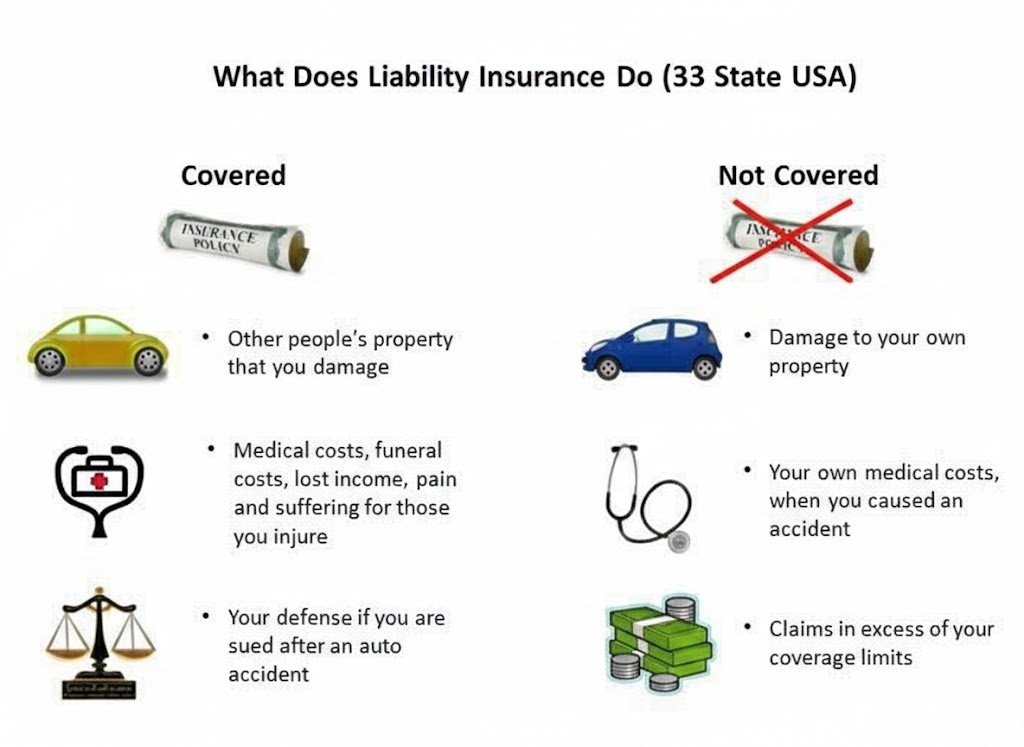

The core of liability coverage is simple: it pays for the other person’s losses. If you are responsible for a car crash, a slip-and-fall on your sidewalk, or a professional mistake that costs a client money, liability insurance steps in.

It handles the bills so you do not have to pay them out of your own pocket. Without it, a single mistake could lead to a lawsuit that lasts for years and results in a judgment that takes every penny you have saved.

Understanding how this works across different regions is vital, as each state has its own rules on the minimum coverage required. While the basics remain the same, the minimum dollar amounts vary widely from state to state.

What Does Liability Insurance Do?

Liability insurance is a type of coverage that helps protect individuals and businesses from the financial burden of legal claims if someone gets injured, their property is damaged, or if you’re considered negligent. Whether you run a small business, work as a freelancer, or operate a company producing goods, liability insurance is crucial in case someone files a claim or lawsuit against you.

This insurance helps cover legal fees, medical bills, and any settlements or awards you may be responsible for. In today’s world, where lawsuits can happen quickly, having liability coverage is not just smart it’s necessary. A single lawsuit could cost thousands or even millions of dollars, potentially threatening the survival of a business or personal finances.

Ultimately, liability insurance safeguards your financial future and gives you peace of mind so you can continue your work without constant worry.

Liability Insurance Types

Liability insurance comes in different forms depending on your profession and the risks involved. Here are the main types:

1. General Liability Insurance

General liability insurance is the most common type for businesses. It protects against claims for bodily injuries, property damage, and personal injuries like slander or libel—both on your business property and as a result of your business activities.

For example, if a customer slips and gets hurt in your store and decides to file a lawsuit, general liability insurance can help cover their medical bills and your legal defense costs.

2. Public Liability Cover

Public liability insurance protects your business from claims made by third parties, such as customers or visitors, who are injured or have property damaged due to your business activities. This is especially important for businesses that interact regularly with the public, like retail stores, restaurants, or event organizers.

While it is sometimes considered a subset of general liability insurance, public liability is usually more focused on accidents involving third parties on your premises or in public spaces.

3. Professional Liability Insurance

Also called Errors and Omissions (E&O) insurance, professional liability is essential for service-based professionals such as consultants, doctors, lawyers, architects, and accountants. It covers claims related to mistakes, negligence, or poor advice.

For instance, if a financial advisor gives bad advice that causes a client to lose money, professional liability insurance can cover the legal costs and damages awarded to the client.

4. Product Liability Coverage

Product liability insurance is crucial for businesses that manufacture, distribute, or sell products. It protects against lawsuits arising from injuries or damages caused by defective or unsafe products.

For example, if your company makes toys and one of them causes harm due to a manufacturing defect, product liability insurance can cover legal fees, settlements, and even the cost of recalling the product.

What Does Liability Insurance Cover?

The coverage varies depending on the policy, but most liability insurance policies protect the following areas:

Personal Injury

Liability insurance can pay for medical bills, rehabilitation, and lost income for someone injured on your property or due to your business activities.

Damage to Property

If your business activities cause damage to someone else’s property, liability insurance usually covers the repair or replacement costs.

Court Fees and Lawyers

Liability insurance covers legal expenses, including attorney fees, court costs, and any settlements or judgments.

Personal and Advertising Injury

This includes non-physical harm such as slander, libel, false advertising, or copyright infringement.

Medical Payments

If someone is hurt on your premises, medical bills can be covered immediately, even without a lawsuit, provided you have liability insurance.

Note: Liability insurance does not cover intentional damage, criminal acts, or property loss to your own business or employees. Those require other types of insurance, like property insurance or workers’ compensation.

Safeguarding Your Assets Through Auto Liability

Auto liability is the most common form of this insurance. In nearly every one of the states mentioned, you cannot legally drive a vehicle without showing proof that you can pay for damages you might cause. This coverage is usually divided into two main parts: bodily injury and property damage.

Bodily injury helps pay for things like hospital stays, surgeries, and even lost wages for the person you hit. Property damage takes care of the costs to fix their car, a fence you might have hit, or even a storefront if the accident was severe.

Experts in the insurance field often suggest that “minimum coverage is rarely enough coverage.” This is because medical costs in the United States have risen much faster than state-mandated insurance limits. If you live in a state where the minimum is only $25,000 for injuries, a single night in a modern hospital could easily surpass that limit. Once the insurance company pays its maximum, you are on the hook for the rest.

Common Components of Auto Liability

- Bodily Injury per Person: The maximum amount paid to one individual hurt in an accident.

- Bodily Injury per Accident: The total amount available if multiple people are hurt.

- Property Damage: The fund used to repair or replace vehicles and physical structures.

- Legal Defense: Most policies also pay for a lawyer if the other driver decides to sue you.

Minimum Auto Liability Requirements in Key States

| State | Bodily Injury (Per Person/Accident) | Property Damage |

| Alabama | $25,000 / $50,000 | $25,000 |

| Arizona | $25,000 / $50,000 | $15,000 |

| California | $15,000 / $30,000 | $5,000 |

| Georgia | $25,000 / $50,000 | $25,000 |

| Illinois | $25,000 / $50,000 | $20,000 |

| North Carolina | $30,000 / $60,000 | $25,000 |

| Ohio | $25,000 / $50,000 | $25,000 |

| Texas | $30,000 / $60,000 | $25,000 |

Protecting the Home with Personal Liability

When you buy a home or rent an apartment, your insurance policy usually includes personal liability. This is often an overlooked part of the policy because people focus on fire or theft. However, personal liability is what protects you if a delivery driver trips on a loose rug in your hallway or if your dog bites a neighbor at the park. This coverage follows you; it does not just stay at your house. If you are on vacation in another state and accidentally cause a fire in a hotel room, your personal liability might cover the damage.

One unique insight into personal liability is the concept of “attractive nuisances.” These are items on your property that might draw children in, such as swimming pools, trampolines, or even large piles of dirt. If a child enters your property without permission and gets hurt using one of these items, you could be held liable. Higher liability limits are often required by insurance companies if you own these features to account for the extra risk.

What Personal Liability Usually Handles

- Medical Expenses: Paying for the immediate care of a guest who gets hurt.

- Property Damage: Fixing a neighbor’s expensive window or electronics broken by you or your kids.

- Lawsuit Costs: Handling the fees for attorneys and court filings.

- Global Coverage: Many policies provide protection even when you are traveling away from home.

Business Liability for Entrepreneurs and Professionals

For those who run a business, liability insurance is the difference between staying open and filing for bankruptcy. General liability insurance covers the “slips and trips” that happen at a place of business. If a customer walks into your store and falls because the floor was wet, they can sue for their medical bills. This insurance covers those costs. It also covers “advertising injury,” which includes things like libel, slander, or using someone else’s idea in your marketing by mistake.

Professional liability, also called errors and omissions, is different. It is for people who give advice or provide a service. If a tax preparer makes a mistake that costs a client thousands in penalties, or an architect designs a building with a structural flaw, general liability won’t help. They need professional liability to cover the financial loss caused by their professional error.

Business Liability Comparison

| Feature | General Liability | Professional Liability |

| Physical Injury | Covers slips, falls, and accidents. | Generally does not cover physical injury. |

| Property Damage | Covers damage to a client’s office or home. | Focuses on financial loss, not physical objects. |

| Work Errors | Does not cover mistakes in professional advice. | Covers errors, omissions, and negligence. |

| Slander/Libel | Included as part of advertising injury. | Often included if related to professional work. |

| Legal Fees | Covered for third-party injury claims. | Covered for claims of professional failure. |

Role of Umbrella Insurance for Extra Security

In many of the thirty-three states where lawsuits are common, a standard policy might not be enough. This is where umbrella insurance comes in. Think of it as a “backup” policy that sits on top of your car and home insurance. If you have a $300,000 limit on your car insurance but get sued for $1 million after a major crash, the umbrella policy pays the remaining $700,000.

This type of insurance is surprisingly affordable because it only pays out after your primary insurance is used up. It is a smart move for anyone with significant savings, a home, or a high income that they want to protect from being taken in a court judgment.

Tips for Managing Liability Risk

- Check Your Limits Yearly: As your wealth grows, your insurance should grow with it.

- Understand Exclusions: Liability insurance almost never covers intentional acts. If you hurt someone on purpose, the insurance company will walk away.

- Document Everything: In a business setting, keep records of safety checks to prove you were not negligent.

- Bundle Policies: Buying your auto, home, and umbrella insurance from one place often gets you a better price and smoother claims.

Common Situations Covered by Liability

- A guest falls off your deck during a summer BBQ.

- You accidentally hit a cyclist while turning at a green light.

- Your small business sends out an email that accidentally uses a copyrighted image.

- An employee at your plumbing company forgets to tighten a pipe, causing a flood in a client’s basement.

Liability insurance is the foundation of financial planning in the United States. By understanding the specific needs of your state and the types of risks you face every day, you can choose a policy that keeps you safe. Whether it is on the road, at home, or at work, having the right amount of coverage ensures that a single bad day does not ruin your entire financial life.

How Does Personal Liability Insurance Differ From Business Liability Insurance?

Personal liability insurance is designed for individuals. It helps cover claims if someone is injured or their property is damaged because of your actions or while on your property. For example, if a guest slips in your home and gets hurt, this insurance can help cover their medical bills or legal costs.

Business liability insurance, on the other hand, is meant for companies and business owners. It protects against similar accidents and also covers risks unique to businesses, such as product defects, recalls, and lawsuits arising from services or operations. Essentially, it’s about keeping your business financially safe while personal liability insurance protects your personal assets.

What Is Umbrella Insurance?

Umbrella insurance is extra liability coverage that extends beyond the limits of your existing policies, such as homeowners, auto, or boat insurance. It’s an affordable way to add extra protection, typically sold in increments of $500,000 or $1 million.

Think of it as a safety net: if a claim exceeds the coverage of your primary policies, umbrella insurance steps in to protect your finances from big, unexpected expenses.

What Is Backdated Liability Coverage?

Normally, liability insurance only covers events that happen after your policy starts. Backdated liability coverage is different it can cover claims that happened before the policy was purchased.

These policies are rare and mostly used by businesses, since personal policies usually don’t offer retroactive coverage. Essentially, it’s a way to protect against past risks that weren’t insured at the time.

What Liability Insurance Covers in 33 States in the USA

- California – Covers bodily injury, property damage, and personal/advertising injury; often requires higher minimums for businesses.

- Texas – Includes general liability, professional, and product coverage; public liability is common for small businesses.

- Florida – Strong focus on bodily injury and property damage; professional liability is important for service industries.

- New York – Covers personal injury, property damage, and legal defense; professional liability often required for consultants and healthcare.

- Illinois – General and product liability widely used; medical payments and legal fees typically included.

- Pennsylvania – Protects against bodily injury, property damage, and court costs; professional liability for services is common.

- Ohio – Covers general, professional, and product liability; personal injury and medical payments included.

- Georgia – Includes general liability and public liability; professional services may need errors and omissions coverage.

- North Carolina – Protects against bodily injury, property damage, and advertising injury; legal defense costs included.

- Michigan – Coverage includes general liability, product liability, and professional liability; medical payments often included.

- New Jersey – Protects against personal and property injury; professional liability is common for legal and healthcare services.

- Virginia – Includes general liability, product, and professional coverage; public liability important for customer-facing businesses.

- Washington – Protects against bodily injury, property damage, and advertising injury; legal fees covered.

- Arizona – General, product, and professional liability covered; medical payments included for on-site accidents.

- Massachusetts – Strong focus on personal injury and property damage; professional liability common in consulting and healthcare.

- Tennessee – Covers bodily injury, property damage, and legal fees; professional liability often required for services.

- Indiana – Includes general liability, product liability, and professional liability; medical payments often included.

- Missouri – Protects against personal injury, property damage, and advertising injury; legal defense costs included.

- Maryland – Coverage includes general, product, and professional liability; medical and court costs often covered.

- Wisconsin – Focus on bodily injury, property damage, and personal injury; professional liability important for consultants.

- Colorado – General and professional liability covered; public liability for businesses with frequent customer interactions.

- Minnesota – Protects against bodily injury, property damage, and advertising injury; medical payments often included.

- South Carolina – Covers general, product, and professional liability; legal fees and settlements included.

- Alabama – Liability insurance protects against personal injury, property damage, and court costs; professional coverage common.

- Louisiana – Includes general, professional, and product liability; public liability important for customer-facing businesses.

- Kentucky – Covers bodily injury, property damage, and legal defense costs; professional liability common for services.

- Oregon – Focus on personal and property injury; professional and product liability included for service and manufacturing businesses.

- Oklahoma – Protects against bodily injury, property damage, and advertising/personal injury; medical payments often included.

- Connecticut – General liability, product, and professional coverage; legal defense and medical payments included.

- Iowa – Protects against bodily injury, property damage, and advertising injury; professional liability common for services.

- Mississippi – Covers general, product, and professional liability; medical payments included for on-site accidents.

- Arkansas – Liability insurance protects against personal injury, property damage, and legal fees; professional coverage often needed.

- Nevada – Includes general, product, and professional liability; public liability important for customer-facing businesses.

FAQ: Question and Answers for Policyholders

What happens if the damage costs more than my insurance limit?

If a court decides you owe more than your policy pays, you are personally responsible for the rest. This could mean the other party can go after your savings, your home, or even a portion of your future paychecks. This is why many people choose limits higher than the state minimum.

Does liability insurance cover my own injuries?

No. Liability insurance only pays for the other person’s medical bills or property damage. To cover your own medical bills after an accident, you would need “Medical Payments” coverage or “Personal Injury Protection” (PIP).

Is liability insurance required for small businesses?

While not every state requires general liability by law (unlike auto insurance), many clients and landlords will refuse to work with you unless you have it. It is also the only thing protecting your business assets if a customer gets hurt on your property.

Does my car insurance cover me if I drive a friend’s car?

Usually, insurance follows the car, not the driver. If you borrow a friend’s car and cause an accident, their insurance usually pays first. However, if their limits are too low, your own liability insurance might act as a secondary backup.

Can I be sued if my dog bites someone outside of my property?

Yes. Most personal liability policies (found in homeowners or renters insurance) cover you and your pets even when you are away from home, such as at a public park.